How NRIs Can File Income Tax Return in India: 2026 Guide

Filing income tax in India as a Non Resident Indian (NRI and OCI card holder) can be confusing. You may struggle to figure out if you must file, what forms to use, or how your foreign and Indian incomes get taxed.

Under Indian tax law, your residential status decides whether you pay tax and what type of income is taxable. Many NRIs miss out on refunds or face penalties because they do not follow the right process.

This guide will show you clear steps for efiling NRI taxes, explain important rules like exemption limits and DTAA benefits, and help you avoid common errors. Get ready to make the next assessment year easy for yourself.

Understand how to file your income tax return with confidence. Read on for each step explained in simple terms.

Key Takeaways

- NRIs must file an Indian income tax return if their total Indian income exceeds ₹2.5 lakh in a financial year, or to claim a refund—this applies even if the bank has already deducted TDS (Section 139 of the Income Tax Act).

- Use ITR-2 if you have salary, house property, or capital gains; use ITR-3 for business or professional income. Double-check your residential status under Section 6 before filing.

- Eligible deductions include up to ₹1.5 lakh under Section 80C (for investments like PPF and ELSS), up to ₹25,000–₹50,000 for health insurance premiums under Section 80D, and education loan interest under Section 80E.

- Claim DTAA benefits to avoid paying double taxes on the same income in India and your country of residence; keep records of all foreign and Indian incomes and tax payments.

- Register on the Income Tax Portal (incometax.gov.in), upload documents such as PAN card, Form 26AS, passport copies, and verify your return using Aadhaar OTP or by mailing a signed acknowledgment within 120 days.

Who is Considered an NRI for Tax Purposes?

A Non-Resident (NRI and OCI card holder), is an individual who resides outside India for a specified period. To determine your status as an NRI for tax purposes, you must evaluate your physical presence in India based on the criteria set in Section 6 of the Income Tax Act.

Determining Residential Status Under Section 6

To determine if you are a Non-Resident Indian for income tax purposes, review Section 6 of the Income Tax Act, 1961. This section states that you qualify as an NRI in the assessment year if you spend less than 182 days in India during the previous financial year.

If your stay is between 60 and 181 days but your total stay over four preceding years does not exceed 365 days, you also fall under Non Residential status.

Stay details require precise tracking through passport stamps and travel records. Only residents get taxed on global income; NRIs pay tax only on Indian-sourced income. Authorities may treat OCI cardholders or PIOs as residents based on these duration rules under Section 6.

Residential Status shapes how much and what type of income gets taxed in India each assessment year.

When Should an NRI File Tax Returns in India?

An NRI should file income tax in India when their total taxable income exceeds the exemption limit set by the government. Filing becomes mandatory for those seeking refunds as well.

To understand your specific situation, explore detailed guidelines on this topic.

Income Threshold for Filing

You must file an Income Tax Return in India for the Assessment Year if your total Indian income exceeds Rs 2.5 lakh during that financial year. This exemption limit applies even if you qualify as a NonResident Indian (NRI) for tax purposes under Section 6 of the Income Tax Act.

For those below age 60, the same threshold applies regardless of residential status.

Interest earned on NRO accounts, rental income from property in India, or short-term capital gains typically count toward this taxable income. If your total taxable Indian income stays below Rs 2.5 lakh and no tax has been deducted at source, filing is not mandatory unless you want to claim a refund or carry forward losses.

Always check current exemption limits as they may change with each Union Budget and Assessment Year updates announced by the Central Board of Direct Taxes (CBDT).

Mandatory Filing for Claiming Refunds

To claim a tax refund, file your Income Tax Return (ITR) even if your Indian income falls below the exemption limit. The Income Tax Department processes refunds only for those who submit their ITR within the due date each Assessment Year.

For example, if banks deducted TDS on interest from NRO accounts and the total taxable income does not cross ₹2.5 lakh, you must complete e-filing to get that money back.

Filing is mandatory to receive any eligible tax refunds as per current Indian tax regulations.

Section 139 of the Income Tax Act mandates this rule for Nonresident Indians (NRIs). Skipping this step can cause delays or forfeiture of your rightful refund. Always provide accurate bank details in India so authorities can credit your refund promptly and securely after processing your return.

Taxable Income for Non Residents

Taxable income for NRIs includes salary, rental earnings, capital gains, and business profits. Each category carries its own tax rules. Familiarize yourself with these classifications to ensure accurate reporting on your return.

For detailed insights into specific types of income and their tax implications, explore further information in this section.

Salary Income

Salary income for NRIs falls under the taxable income category in India. If you earn a salary from an Indian employer or through services rendered in India, this income is subject to taxation.

Tax rates for salaried individuals depend on your total earnings and applicable tax slabs set by the government.

You must report all salary income while filing your Income Tax Return (ITR). This applies even if you have earned part of it outside India. Take note of any deductions available to reduce your taxable amount, such as contributions to retirement funds or specified investments.

Maintain records of all payslips and employment contracts for accurate reporting during the filing process.

Income from House Property

Income from house property falls under taxable income for NRIs in India. If you own a property, rental income qualifies as taxable. You must report any rent collected if you earn it while residing outside of India.

The Income Tax Act states that the net annual value of your property determines tax liability.

You can deduct certain expenses while computing this income. Deduct municipal taxes and maintenance charges from your total rental income. The standard deduction of 30% applies to your net annual value, covering repairs and other costs associated with the property’s upkeep.

Knowing these deductions helps you calculate your taxable amount accurately, leading to better financial planning for future gains or losses from capital assets such as real estate investments.

Next, explore how salary income is taxed for NRIs in India.

Income from Capital Gains

Capital gains arise when you sell an asset for more than its purchase price. NRIs pay tax on these gains based on how long they held the asset. Short-term capital gains occur if you hold an asset for less than 36 months or 12 months for specific assets like shares and mutual funds.

The government taxes these short-term gains at a rate of 15%.

Long-term capital gains apply to assets held longer than the specified period. Gains above INR 1 lakh in a financial year are subject to taxation at 20% with indexation benefits, which help reduce your overall taxable amount.

Understanding this distinction allows you to enhance your tax planning effectively, especially when dealing with properties or investments in India. Next, explore deductions and exemptions available for NRIs.

Income from Business and Profession

Income from business and profession falls under the taxable income for NRIs in India. You must report this income while filing your tax return. The Income Tax Act defines how you should calculate your profits, deduct expenses directly connected to generating that income, and maintain proper records.

If you earn through a business or profession in India, ensure to keep accurate financial statements throughout the year. This documentation helps establish your taxable income accurately.

Declare all applicable revenues and ensure compliance with Indian tax regulations.

Income from Other Sources

From your business and profession income, you may also earn money from other sources. Taxable income includes interest from bank deposits, dividends from shares, and any winnings from lotteries or gambling.

These earnings fall under “Income from Other Sources.” The Indian tax system requires you to report this income while filing your tax return in India. Ensure you include all relevant amounts to stay compliant with regulations.

You can claim deductions for expenses related to earning this income as permitted by law. Make sure you check the applicable tax slabs for accurate calculations of your total taxable amount.

Deductions and Exemptions for NRIs

Non-Resident Indians can benefit from various deductions and exemptions, such as those under Section 80C for investments or health insurance premium deductions under Section 80D. Explore these options to reduce your taxable income effectively.

Deductions Under Section 80C

Section 80C allows you to claim deductions on specific investments and expenses. You can reduce your taxable income by up to INR 1.5 lakh through qualifying contributions. Eligible options include Public Provident Fund (PPF), National Pension Scheme (NPS), Equity-Linked Savings Scheme (ELSS), and life insurance premiums.

Investing in these instruments supports tax savings and promotes long-term financial security. Ensure that you keep records of all investment receipts, as they may be needed when filing your income tax return in India.

Take advantage of this deduction to lower your overall tax liability while securing your future.

Deduction for Health Insurance Premiums (Section 80D)

Claim a deduction for health insurance premiums under Section 80D. You can reduce your taxable income by paying for health insurance coverage. NRIs can deduct premiums paid for themselves, their spouse, children, and parents.

The deduction limit varies based on the insured’s age. If you’re below 60 years old, you can claim up to ₹25,000. If your parents are also covered and they are above 60 years old, you can claim an additional ₹50,000.

Understanding these limits helps in maximizing your deductions effectively. Next, explore the deductions available under education loans in Section 80E.

Deduction for Education Loans (Section 80E)

Section 80E allows you to claim deductions on interest paid for education loans. This deduction applies to loans taken for higher studies, including courses in India and abroad. You can claim these deductions for a maximum of eight years or until the interest is fully repaid.

Ensure that you have clear documentation from your lending institution. The bank’s interest statement must specify the amount paid during the financial year. You do not need to submit this document along with your tax return but keep it handy in case of inquiries.

Section 80E provides a significant benefit for NRIs pursuing educational opportunities, allowing them to reduce their taxable income effectively.

Moving forward, familiarize yourself with exemptions on capital gains from property sales next.

Exemptions on Capital Gains from Property Sale

Deductions for education loans lead to important exemptions on capital gains from property sales. As a Non-Resident Indian (NRI), you benefit from certain exemptions when selling property in India.

If you sell residential or commercial real estate, you can claim tax exemptions under specific conditions.

You can exempt capital gains if you reinvest in another residential property within two years of the sale. Investing in bonds specified by the government under Section 54EC offers another way to reduce your taxable income.

Keeping records of the purchase price and expenses related to improvements will help maximize your deductions and ensure compliance with Indian tax regulations.

How To File NRI Income Tax Online (Steps Explained)

To file income tax as an NRI, you must first register or log into the Income Tax Portal. Then, select the appropriate ITR form based on your income type and provide all necessary documents for a smooth filing process.

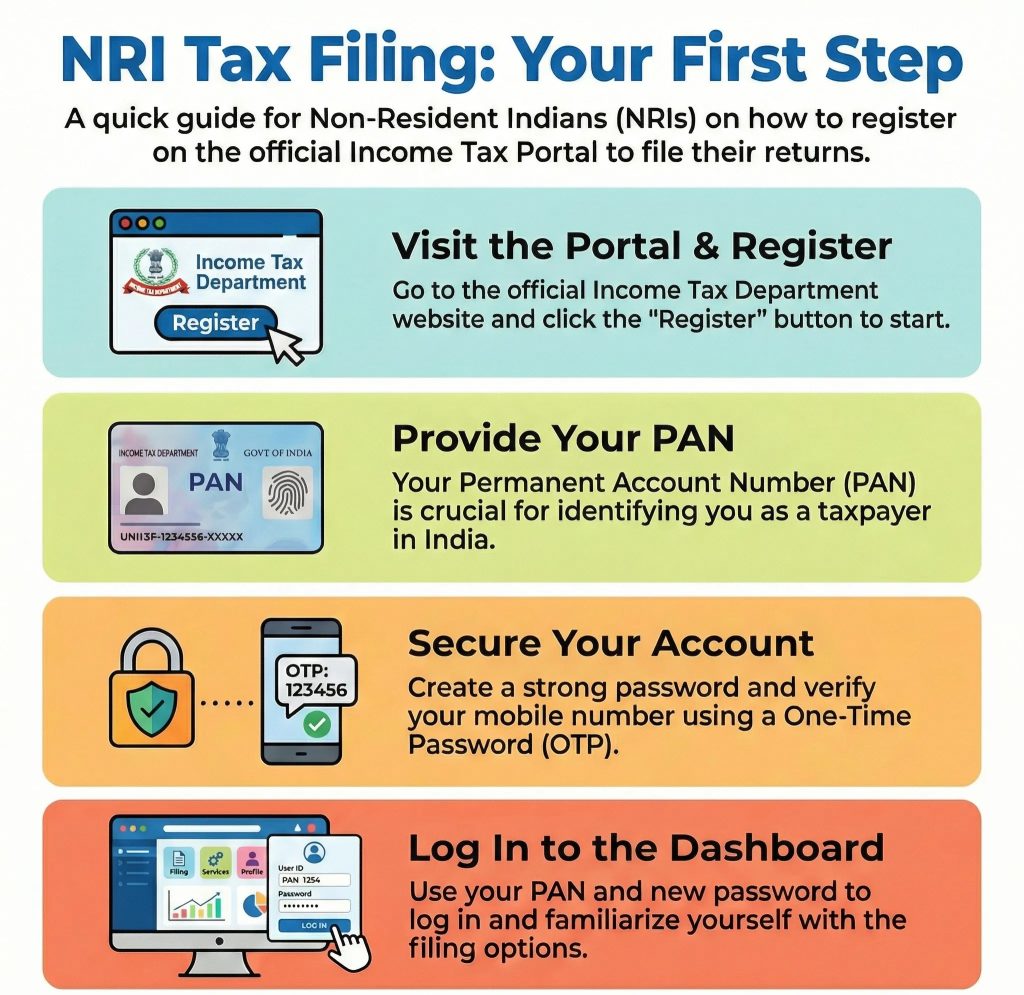

Registering or Logging into the Income Tax Portal

You must register or log into the Income Tax Portal to file your income tax. This step ensures you can manage your tax filing process efficiently.

- Visit the official Income Tax Department website. Look for a link that allows you to access the Income Tax Portal.

- Click on “Register” if you do not have an account yet. Fill in your basic details such as your name, date of birth, and email address.

- Provide your Permanent Account Number (PAN). This is crucial since it identifies you as a taxpayer in India.

- Choose a strong password for your account. A secure password protects your information from unauthorized access.

- Verify your mobile number using an OTP (One-Time Password). The portal will send an OTP to the number you provide; enter this code to complete verification.

- Log into the portal with your PAN and newly created password if you already have an account. Make sure that all input fields are correct before submitting.

- Browse through the dashboard after logging in. Familiarize yourself with available options, including filing returns and checking status.

Understanding these steps helps streamline the tax filing process for NRIs in India. Next, let’s explore the appropriate ITR forms you should select for filing returns in India.

Selecting the Appropriate ITR Form (ITR-2 or ITR-3)

Selecting the correct ITR form is crucial for your income tax filing as an NRI. It determines how you report your income and claim deductions or exemptions.

- ITR-2: Use this form if you earn income from salary, house property, or capital gains. You also qualify if you have foreign income but do not run a business in India. Download ITR-2 form here.

- ITR-3: Choose this form if you have income from a business or profession in India. It accommodates detailed reporting of various income streams and expenses related to your business operations. Get ITR-3 form here.

- Check Eligibility: Review each form’s eligibility criteria carefully. Ensure that your profile fits the requirements before selecting a form for filing.

- Gather Documentation: Collect all necessary documents that support your income claims. This includes Form 16 for salary, rental agreements, and proof of capital gains.

- Online Filing: Access the Income Tax e-filing portal to submit the chosen ITR form electronically. This process simplifies submissions and reduces paperwork.

- Double-check Information: Ensure all details entered in the ITR are accurate and complete to avoid issues later on, such as rejections or penalties.

- Seek Professional Advice: Consider consulting with a tax professional if unsure about which form suits your situation best; their expertise can prevent costly mistakes during tax filing.

- Track Your Filing Status: After submission, monitor your filing status on the portal to verify successful completion and address any follow-up actions promptly.

Providing Necessary Documents

To file your income tax in India as a Non-Resident Indian (NRI), you need to gather specific documents. These documents support your tax return and ensure compliance with Indian tax regulations.

- Valid Passport: Your passport serves as proof of identity and residency status. Ensure it is current and reflects accurate personal information.

- Permanent Account Number (PAN): Obtain a PAN if you do not have one, as it is mandatory for filing income tax returns in India.

- Form 26AS: Access this document from the Income Tax Department’s website. It shows details about taxes deducted at source (TDS) on your income. You can view 26AS form here.

- Bank Statements: Collect bank statements that reflect all transactions. This documentation helps verify your income sources and amounts received during the financial year.

- Salary Certificates: If you earn a salary, obtain certificates from your employer detailing your earnings, TDS deductions, and other allowances.

- Rental Agreements: For rental income, secure copies of agreements for properties you rent out. This verifies property ownership and rental amounts collected.

- Capital Gains Statements: Gather statements related to capital gains if you sold assets or investments during the assessment year. Document sale proceeds and acquisition costs clearly.

- Insurance Premium Receipts: Compile receipts for health insurance premiums paid under Section 80D to claim deductions effectively.

- Education Loan Documents: Maintain records of education loans if claiming deductions under Section 80E; this should include loan sanction letters and payment receipts.

- Any Other Relevant Documents: Include any additional paperwork that establishes other sources of income or eligible deductions relevant to your financial situation.

Ensure these documents are complete before starting the filing process to avoid complications later on and promote accurate reporting of taxable income in accordance with Indian tax laws.

Verifying the Filed Return (Aadhaar OTP or Physical Verification)

You must verify your filed return after completing the process. This step ensures that your Income Tax Return (ITR) is processed correctly.

- Use Aadhaar OTP for verification. If you have linked your Aadhaar number with your PAN, select this option on the portal. You will receive a one-time password (OTP) on your registered mobile number. Enter the OTP in the designated field to confirm your identity.

- Choose physical verification if you prefer not to use Aadhaar OTP. This requires you to sign a hard copy of your ITR acknowledgment form. Mail this signed copy to the Centralized Processing Center (CPC) within 120 days of filing.

- Maintain a record of your verification method. Keep all communication and acknowledgment receipts safe for future reference.

- Ensure timely verification to avoid delays in processing your return or receiving any tax refund due to you. Completing this step confirms compliance with Indian tax regulations.

- Keep track of deadlines related to income tax filings and verifications as specified by the Income Tax Department each assessment year.

Following these steps helps ensure that your ITR remains valid, securing proper handling of taxes and any potential refunds from Indian authorities.

Key Considerations While Filing ITR as an NRI

Key considerations include understanding Double Taxation Avoidance Agreements (DTAAs). These agreements help you avoid paying taxes in two countries on the same income. TDS applies to your NRI income, so keep track of any deductions from your earnings.

Advance tax payments may also be necessary based on your total income for the financial year.

Double Taxation Avoidance Agreement (DTAA) Benefits

The Double Taxation Avoidance Agreement (DTAA) offers significant advantages for Non-Resident Indians (NRIs). With this agreement, you can avoid being taxed on the same income in both India and your country of residence.

This benefit reduces your overall tax liability.

Essentially, if you earn income in India while residing abroad, DTAA ensures that you only pay taxes to one nation. It also allows you to claim a credit for taxes paid overseas against your Indian tax liability.

As a result, this framework promotes financial compliance and eases the burden of double taxation on NRIs filing their income tax returns in India.

TDS on NRI Income

TDS, or Tax Deducted at Source, applies to your income in India. As an NRI, you face TDS on several types of income. For example, salary payments attract TDS at a rate specified by the Indian tax department.

Income from property rentals also incurs TDS; landlords withhold this amount before passing the rest to you.

You must keep track of these deductions throughout the year because they affect your final tax liability. If excess TDS gets deducted, you can claim a refund when filing your income tax return (ITR).

Understanding your obligations concerning TDS helps ensure compliance with Indian tax regulations while optimizing your financial outcomes in India.

Handling Advance Tax Payments

Advance tax payments require careful planning for NRIs. You must pay this tax if your total income exceeds Rs 10,000 in a financial year. Calculate your expected income and determine the amount you owe.

Due dates for advance tax payments fall on June 15, September 15, December 15, and March 15.

Make sure to remit these payments online or through authorized banks. Keep records of transactions as they support your filings later. This systematic approach aids in timely compliance with Indian tax regulations and reduces penalties associated with late payments.

Next, consider common mistakes to avoid during the filing process for greater accuracy and peace of mind.

Common Mistakes to Avoid

Filing income tax as an NRI involves several key steps. Many NRIs overlook the importance of verifying their residential status before filing. This mistake can lead to incorrect tax assessments and unexpected liabilities.

Ensure you understand whether you qualify as a resident or non-resident based on your stay in India.

Failing to select the correct ITR form is another common error. Choosing the wrong form can delay your return processing or result in penalties. Always check if you’re eligible for ITR-2 or ITR-3 based on your income sources.

Missing deadlines also complicates matters, so mark important dates clearly in your calendar to avoid late filing fees or penalties associated with delayed submissions.

Benefits of Filing Income Tax for NRIs

Filing income tax in India offers several key benefits for Non-Resident Indians (NRIs). It helps you maintain adherence to Indian tax regulations. Adherence avoids penalties and legal issues related to tax evasion or non-filing.

You can also claim refunds on excess taxes paid. Many NRIs may not realize that they qualify for a refund if they fall below the taxable income threshold. Furthermore, filing allows you to access certain financial products in India, like loans or bank accounts, which often require proof of filing your income tax return.

Conclusion

Filing income tax in India as an NRI does not have to be stressful if you understand the rules and follow the correct steps. Your residential status, type of income, applicable ITR form, and use of deductions or DTAA benefits all play a direct role in how much tax you pay—or how much refund you receive.

At NRIinvestIndia.com, we have worked with NRIs across multiple countries since 2007 and have seen the same issues repeat every year—missed refunds, wrong ITR forms, unclaimed DTAA benefits, and avoidable notices due to simple mistakes. Most of these problems arise not because the law is unclear, but because the process is misunderstood or rushed.

If you review your residential status each year, keep proper records, report only Indian-source income, and verify your return on time, you stay compliant and avoid unnecessary penalties. Filing correctly also helps you maintain a clean tax record in India, which is often required for future investments, property transactions, or remittances.

With the right preparation, income tax filing for NRIs can be handled smoothly and confidently—year after year.

FAQs

1. What is the process for an NRI to file income tax in India?

An NRI must follow these steps: determine taxable income, gather necessary documents, fill out the appropriate tax return form, and submit it online or at a designated office.

2. Which forms should NRIs use to file taxes in India?

NRIs typically use Form ITR-1 or ITR-2 based on their income sources. These forms are available on the Income Tax Department’s website.

3. Are there any specific deductions available for NRIs filing taxes in India?

Yes, NRIs can claim deductions under sections such as 80C for investments and 80D for health insurance premiums. It is essential to keep proper documentation of these claims.

4. How can an NRI pay their income tax due in India?

An NRI can pay taxes online through the Income Tax Department’s portal using net banking or by visiting authorized banks that accept tax payments.