How to Invest in Indian Stock Market as an NRI in 2026: Complete PIS Guide

For millions of non-residents (NRIs, OCI cardholders, and PIOs), investing in India’s stock market has never been more accessible — or more rewarding. India remains one of the world’s fastest-growing major economies, and Budget 2026 just doubled the individual NRI investment cap in listed Indian companies to 10%. Yet most NRIs either don’t know where to start or are held back by confusion around accounts, compliance, and tax.

This guide cuts through all of it. Whether you are based in the USA, UAE, UK, or Canada, you will find everything you need here — from opening the right accounts to understanding your tax position — to start investing in Indian stocks legally, confidently, and profitably.

Can NRIs Invest in the Indian Stock Market?

Yes. NRIs, OCI cardholders, and PIOs can legally invest in Indian listed stocks through the RBI’s Portfolio Investment Scheme (PIS) or the Non-PIS route. You need an NRE or NRO bank account, PIS permission from a designated bank, and a linked demat and trading account with a SEBI-registered broker. Budget 2026 doubled the individual NRI investment cap to 10% of a company’s paid-up capital. The right to do so is governed by the Foreign Exchange Management Act (FEMA) 1999, specifically under Schedule 3 of the FEMA Non-Debt Instruments Rules, 2019, which grants NRIs access to Indian listed equities through the RBI’s Portfolio Investment Scheme.

Three regulatory bodies oversee every NRI stock market transaction in India:

- RBI — manages capital flows, PIS permissions, and NRE/NRO account rules

- SEBI — regulates brokers, KYC norms, and market conduct

- FEMA — sets the overarching legal framework for all cross-border investments

Understanding which body governs which part of your investment journey will save you from costly compliance mistakes.

Who Qualifies as an NRI for Investment Purposes?

Under FEMA 1999, you are classified as an NRI if you are an Indian citizen who has stayed outside India for more than 182 days in a financial year, or if you have gone abroad for employment, business, or any purpose indicating an indefinite stay outside India.

This matters because your investment rules, tax treatment, and repatriation rights all flow directly from your FEMA residential status — not your passport, and not your visa type.

What About OCI Cardholders and PIOs?

- OCI cardholders — treated largely on par with NRIs for investment purposes. They can participate in PIS and invest in listed Indian companies subject to the same caps that apply to NRIs. However, like NRIs, they cannot invest in agricultural land or plantation property.

- PIOs without OCI status — may face additional documentation requirements and certain scheme-specific restrictions. If you are a PIO without an OCI card, verify your access with your bank and broker before assuming NRI-equivalent rights.

- Foreign nationals with no Indian origin — cannot access PIS. They must invest through the Foreign Portfolio Investor (FPI) route, regulated separately by SEBI.

⚠️ If you hold a foreign passport but have Indian-origin parents or grandparents, check whether you qualify for an OCI card — it significantly expands your investment access in India.

What Did Budget 2026 Change for NRI Investors?

Budget 2026 introduced the most significant reform to NRI equity investment rules in over a decade. The individual investment limit for NRIs in any single listed Indian company was doubled from 5% to 10% of its paid-up capital. The aggregate cap for all NRIs collectively in a single company was raised from 10% to 24%.

This reform was driven by the need to attract NRI capital at a time when foreign institutional investors pulled out heavily from Indian equities in 2025 and early 2026. Market analysts project incremental NRI inflows of USD 3–4 billion in FY2027 as a direct result.

What this means practically for you:

- You can now build a meaningful stake in a single listed Indian company — up to 10% of its total shares

- Mid-cap and small-cap companies, where 10% represents a sizeable holding, become far more accessible

- Expatriate professionals can now participate more directly in employee stock option plans without complex trust structures

For broader context, read our guide on why NRIs are investing in India and how to invest in India as an NRI.

PIS vs Non-PIS — Which Route Is Right for You?

Now that you know you can invest, the first real decision is choosing your route. The RBI provides two pathways for NRIs to invest in Indian listed equities, and picking the wrong one creates tax headaches and compliance issues down the line.

What Is the Portfolio Investment Scheme (PIS)?

The Portfolio Investment Scheme is an RBI-regulated channel that allows NRIs and OCI cardholders to purchase and sell shares and convertible debentures of Indian companies on a recognised stock exchange. Under PIS, all your transactions flow through a single designated bank account — either NRE or NRO — that holds a PIS permission letter issued by the RBI through your bank.

Every buy and sell transaction is reported to the RBI by your designated bank. TDS is automatically deducted at source on gains. This makes PIS the most compliant and auditable route for NRI equity investing — and it is the only route that gives you full repatriation rights on your profits when using an NRE account.

What Is the Non-PIS Route?

The Non-PIS route allows NRIs to invest in Indian equities without PIS permission, using their NRO account directly. It is simpler to set up — no PIS letter required — but it comes with meaningful trade-offs.

Under Non-PIS, you cannot trade equity derivatives (F&O) and repatriation of proceeds is capped. Tax reporting becomes your responsibility rather than being auto-handled by the bank. Non-PIS works best for NRIs who want to invest in mutual funds, use IPO applications, or hold existing pre-NRI equity portfolios in an NRO account.

PIS vs Non-PIS — Side by Side

| Feature | PIS Route | Non-PIS Route |

|---|---|---|

| RBI permission required | Yes | No |

| Bank account needed | NRE or NRO (designated) | NRO only |

| Equity delivery trading | ✅ Yes | ✅ Yes |

| Intraday trading | ❌ Not allowed | ❌ Not allowed |

| F&O / Derivatives | ❌ Not allowed | ❌ Not allowed |

| TDS deduction | Auto by bank | Self-managed |

| Full repatriation | ✅ Via NRE-PIS | ❌ Capped at $1M/year via NRO |

| Best for | Long-term equity investors | Mutual funds, IPOs, legacy holdings |

Can You Use Both Routes at the Same Time?

You can — but with an important restriction. You cannot hold PIS and Non-PIS equity positions through the same demat account. If you are using PIS through your NRE account for listed stocks, any Non-PIS holdings (such as mutual fund units) must be held separately. Your broker and bank will guide you on segregating these at account opening.

For most NRIs reading this — particularly those based in the USA, UAE, UK, or Canada with surplus income to invest regularly — the PIS route via an NRE account is the right choice. Full repatriation, cleaner tax records, and RBI compliance in one structure.

Read our detailed guide on NRE and NRO accounts for NRIs to understand the banking side before proceeding to account setup.

NRE vs NRO Account — Which One Do You Need for Stock Trading?

Once you have decided to go the PIS route, your next decision is which account type to link it to. This choice determines whether your profits can be freely sent back to your country of residence — so it is worth getting right before you open anything.

NRE Account for Stock Trading

An NRE (Non-Resident External) account holds funds you remit from abroad, converted into Indian rupees. When linked to PIS, it is the most powerful setup for NRI equity investing. Interest earned is tax-free in India, and both the principal and profits from stock sales are fully and freely repatriable — meaning you can send them back overseas without any annual cap or RBI approval.

This is the account most NRIs based in the USA, UAE, UK, and Canada should be using as their primary PIS account.

NRO Account for Stock Trading

An NRO (Non-Resident Ordinary) account is designed for income you earn within India — rent, dividends, pension, or proceeds from selling Indian assets. It can be linked to PIS, but repatriation is capped at USD 1 million per financial year, and interest earned is subject to TDS at 30% (reducible under DTAA with your country of residence).

How to Start Investing in Indian Stocks as an NRI — Step by Step

Setting up your NRI stock investment structure takes a little patience upfront, but once the accounts are linked and KYC is done, the entire process runs seamlessly from wherever you live in the world. Here is the exact sequence to follow.

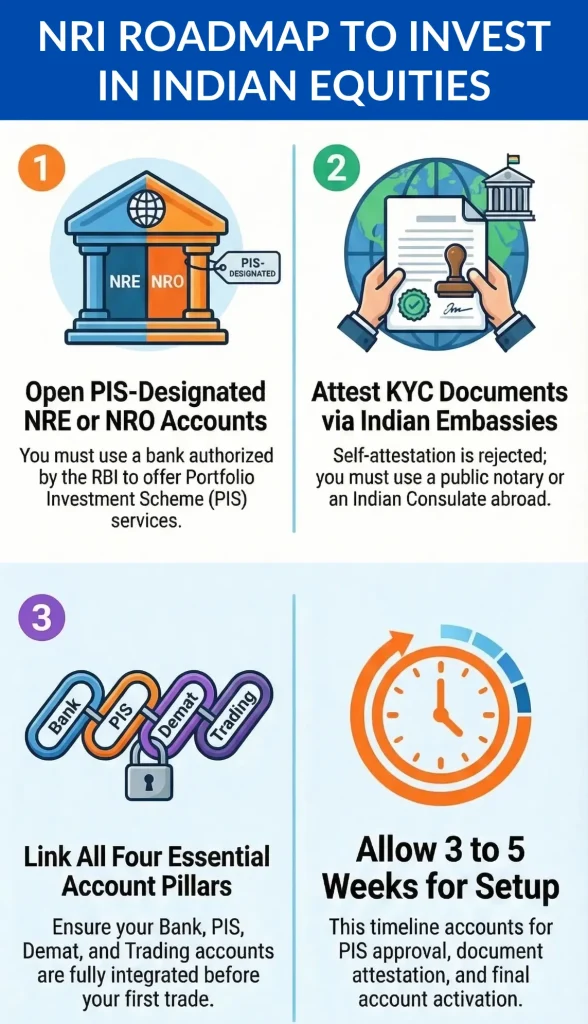

Step 1: Open an NRE or NRO Bank Account With a PIS-Designated Bank

Your first move is opening an NRE account (for repatriable investing) or NRO account with a bank that is authorised by the RBI to offer PIS services. Major PIS-designated banks include HDFC Bank, ICICI Bank, Kotak Mahindra Bank, Axis Bank, IDFC First Bank, SBI, and IndusInd Bank.

If you already have an NRE or NRO account with one of these banks, you can apply for PIS permission directly without opening a new account.

Step 2: Apply for PIS Permission

Once your NRE or NRO account is active, request a PIS permission letter from your designated bank. The bank applies to the RBI on your behalf — this is now largely a paperless process at most major banks and is approved within 2 to 5 working days. You will receive a PIS letter that must be submitted to your broker at the next step.

Note: You can only hold PIS permission with one bank at a time. If you switch banks later, your old PIS must be surrendered before the new one is activated.

Step 3: Choose a SEBI-Registered Broker

Select a broker that explicitly supports NRI accounts. Not all brokers do. Look for one that offers:

- NRE-PIS and NRO-PIS account compatibility

- Online account opening with Video In-Person Verification (V-CIP)

- Clear NRI brokerage pricing (rates often differ from resident accounts)

- Dedicated NRI support team

Popular NRI-friendly brokers include Zerodha, ICICI Direct, HDFC Securities, Kotak Securities, and Angel One.

Step 4: Submit Your NRI KYC Documents

SEBI requires NRIs to submit a specific set of KYC documents for both trading and demat account opening. IndiaStat Here is the complete checklist:

Identity & Status Documents:

- Valid passport (all pages with photo and signature)

- Valid visa or resident permit of your country of residence

- OCI card or PIO card (if applicable)

- PAN card — mandatory, no exceptions

Address Proof:

- Overseas address proof — any one of: driver’s licence, national ID, utility bill (not older than 3 months), overseas bank statement, or council tax bill

- Indian address proof — passport, Aadhaar (optional for NRIs), or any government-issued document with Indian address

Banking & Investment Documents:

- NRE or NRO bank account proof (cancelled cheque or bank statement)

- PIS permission letter from your designated bank

- FATCA/CRS declaration — mandatory for residents of USA, UK, Canada, Australia, and 100+ countries under automatic information exchange agreements

- Passport-sized photograph with signature across the photo

⚠️ All KYC documents must be attested by one of the following: an authorised official of an overseas branch of an Indian scheduled commercial bank, a public notary abroad, a court magistrate or judge abroad, or the Indian Embassy or Consulate General in your country of residence. IndiaStat Self-attestation alone is not accepted for NRI accounts.

Step 5: Open Your Demat Account

Your demat account is where your shares are held electronically. It is opened with a Depository Participant (DP) — which is usually your broker or bank — registered with either NSDL (National Securities Depository Limited) or CDSL (Central Depository Services Limited). Both are equally reliable.

Once your KYC is registered with a SEBI-registered KYC Registration Agency (KRA), you do not need to repeat the KYC process each time you open a new investment account. Finedge Your KYC is portable across all SEBI-registered brokers and mutual fund platforms in India.

Step 6: Link All Four Accounts

This is the step most NRIs miss — and it is critical. All four accounts must be correctly linked:

NRE/NRO Bank Account → PIS Permission → Demat Account → Trading Account

Your bank, broker, and depository participant will coordinate this linking. Confirm in writing that the linkage is complete before placing your first trade. Any break in this chain can cause transactions to fail or be flagged as non-compliant.

Step 7: Fund Your Account and Place Your First Trade

Transfer funds from your overseas account into your NRE or NRO bank account. Once the funds are reflected, you are ready to buy listed Indian equities through your trading account. All settlements happen in Indian rupees through your designated PIS bank account, with TDS automatically deducted on any gains at the point of sale.

How Long Does the Entire Process Take?

| Stage | Typical Timeline |

|---|---|

| NRE/NRO account opening | 5–10 working days |

| PIS permission approval | 2–5 working days |

| Demat + trading account activation | 5–10 working days |

| Document attestation (if overseas) | 3–7 working days |

| Total end-to-end | 3 to 5 weeks |

Starting early is key. Most NRIs who delay this process do so because they underestimate the document attestation time — especially those in countries where Indian consulates have longer appointment queues.

If you do not yet have a PAN card, get that sorted first — read our complete guide on how to apply for a PAN card as an NRI.

What Can NRIs Buy and Sell on Indian Stock Markets?

Now that your accounts are set up, it helps to know exactly which instruments are open to you — and which are off-limits. The rules here are governed jointly by FEMA 1999, RBI guidelines, and SEBI regulations, and they are non-negotiable.

Permitted Instruments for NRI Investors

NRIs and OCI cardholders can invest in the following instruments through the PIS route:

- Listed equity shares on BSE or NSE — delivery-based only

- Convertible debentures of listed Indian companies

- Exchange Traded Funds (ETFs) — equity and index ETFs only (not currency or commodity ETFs)

- IPOs (Initial Public Offerings) — you can apply through your NRE or NRO account

- Rights issues and bonus shares of companies you already hold

- Warrants and partly paid shares of listed companies

Prohibited Sectors Under FEMA and RBI Rules

NRIs are strictly prohibited from investing in chit funds, Nidhi companies, agricultural or plantation activities, and real estate trading — though buying a home for personal use is permitted. IndiaStat

The complete prohibited list for NRI equity investors:

| Prohibited Sector | Reason |

|---|---|

| Chit funds | RBI policy — unregulated informal finance |

| Nidhi companies | Deposit-taking NBFCs excluded from foreign investment |

| Agricultural businesses | FEMA restriction on farmland and plantation activities |

| Real estate trading | Buying/selling property as a business (personal home purchase allowed) |

| Lottery businesses | RBI restricts this for national security and policy reasons Finedge |

| Gambling and betting | Prohibited sector under FDI policy |

| Atomic energy | Strategic sector — government controlled |

| Railway operations | Public sector exclusion |

| Print media | Government route required; effectively closed to NRI retail investors |

⚠️ Your broker’s trading platform will automatically block purchase orders for companies under a sectoral ban. RBI and SEBI publish and update this list regularly. If you are unsure about a specific stock, check with your broker before placing an order.

Investment Limits — The 10% Cap Explained

Under the reforms introduced in Budget 2026, an individual NRI can now hold up to 10% of the paid-up capital of any single listed Indian company. The aggregate cap — meaning the combined holding of all NRIs and OCIs together in one company — is 24% of paid-up capital.

What this means in practice: if a company has issued 1 crore shares, you as an individual NRI can hold up to 10 lakh of those shares. Once aggregate NRI holding in a company approaches the 24% ceiling, RBI notifies the stock exchanges and further purchases are halted automatically — your broker will alert you.

A company’s board can pass a resolution to raise the aggregate NRI cap from 24% up to the applicable sectoral FDI limit — but that is a company-level decision, not something individual investors control.

Can NRIs Trade Futures and Options (F&O)?

This is one of the most frequently asked — and most misunderstood — questions. The short answer is: effectively no, not through the standard PIS route.

NRIs may participate in derivatives under strict conditions — margins must be brought from abroad and positions must be closed before expiry — but such participation is rare and subject to individual broker and exchange approval. Finedge Most NRI-designated broker platforms do not offer F&O access at all, and attempting to trade derivatives without explicit approval is a SEBI violation.

If derivatives exposure to Indian markets is something you specifically need, speak to a SEBI-registered investment advisor about the FPI route — a separate and significantly more complex structure.

Is Intraday Trading Allowed for NRIs?

No — and this is absolute. NRIs are limited to delivery-based trades only. Intraday trading, short selling, and margin trades are prohibited to comply with RBI and SEBI frameworks. IBEF You must take delivery of shares you purchase and hold them for at least one trading day before selling.

All equity trades must be settled on a delivery basis. Short selling and derivatives trading are not permitted under PIS. Bajajlifeinsurance Attempting intraday trades through an NRI account can result in the trade being reversed, your account being flagged, and potential FEMA penalties — which can be as high as three times the contravention amount.

For NRIs who want market exposure without stock-picking, Indian mutual funds offer a compliant and diversified alternative — read our guide on NRI mutual fund investments in India.

Tax on NRI Stock Market Gains in India — 2026 Rates

Understanding your tax position before you invest is not optional — it is what separates NRIs who build wealth from those who get unpleasant surprises at the end of the financial year. The good news is that the framework, once understood, is predictable and manageable.

Short-Term Capital Gains (STCG)

If you sell listed equity shares within 12 months of purchase, your gains are classified as short-term. As of 2026, STCG on listed equity is taxed at a flat rate of 20% Finedge, plus applicable surcharge and health and education cess — bringing the effective rate slightly higher depending on your total Indian income. No indexation benefit is available, and no basic exemption limit applies to NRIs on this income.

Long-Term Capital Gains (LTCG)

Hold your shares for more than 12 months and the tax treatment improves considerably. Listed equity shares held for more than 12 months qualify as long-term capital gains, with profits exceeding ₹1.25 lakh taxed at 12.5% annually. Indexation benefits are not available. PolicyBazaar

This makes the holding period decision one of the most financially significant choices you will make as an NRI equity investor. Selling a week before the 12-month mark at 20% versus a week after at 12.5% on gains above ₹1.25 lakh can mean a meaningful difference in your net return — especially on larger positions.

How TDS Works on Your PIS Account

This is where the PIS structure earns its value. NRIs face mandatory Tax Deducted at Source on their equity gains — unlike resident Indians who self-declare. For LTCG, brokers deduct TDS at 12.5% on gains exceeding the exemption limit. Mintbyte For STCG, TDS is deducted at 20%.

The deduction happens automatically through your designated PIS bank at the time of each sale settlement. You receive the net proceeds in your NRE or NRO account after TDS. This means your compliance burden on routine stock trades is minimal — the bank handles the reporting to the RBI and the tax department simultaneously.

One important note: if you do not provide a valid PAN to your broker, Section 206AA of the Income Tax Act pushes TDS to 20% or higher regardless of the applicable rate. Khaleej Times Always ensure your PAN is correctly linked to your trading account before your first transaction.

If your actual tax liability is lower than the TDS deducted — for example, because your gains fall below the ₹1.25 lakh LTCG exemption — you can reclaim the excess by filing an ITR in India.

DTAA — How to Avoid Being Taxed Twice

India has Double Taxation Avoidance Agreements with over 90 countries. Under DTAA, NRIs can pay taxes in one country and claim an exemption in the other — or pay in both and claim relief for taxes already paid in the other country. Bajajlifeinsurance For NRIs in countries with no capital gains tax — such as the UAE — this is particularly valuable, as Indian tax paid is your final liability with no further obligation at home.

Here is how DTAA applies for NRIs in the four largest diaspora countries:

| Country | Capital Gains Tax at Home | DTAA with India | Practical Outcome |

|---|---|---|---|

| USA | Yes — federal + state CGT | Yes (India-US DTAA) | Claim foreign tax credit in US for tax paid in India |

| UAE | No capital gains tax | Yes (India-UAE DTAA) | Indian tax is final — no double taxation |

| UK | Yes — CGT applies | Yes (India-UK DTAA) | Claim credit for Indian tax against UK CGT liability |

| Canada | Yes — 50% inclusion rule | Yes (India-Canada DTAA) | Claim foreign tax credit; consult CA on treaty rates |

To claim DTAA benefits, you must submit two documents to your Indian broker or bank:

- Tax Residency Certificate (TRC) — issued by the tax authority in your country of residence

- Form 10F — a self-declaration form filed on the Income Tax India e-portal

⚠️ Obtain your TRC and submit Form 10F before the financial year ends — delays can prevent DTAA claims for that year’s transactions. Khaleej Times

Do NRIs Need to File an ITR in India for Stock Market Gains?

If the correct TDS has already been deducted on your equity gains, you are not obligated to file an Indian ITR unless you wish to claim a refund or report additional Indian income. PolicyBazaar However, filing is strongly recommended in three situations:

- Your TDS deducted exceeds your actual tax liability (claim a refund)

- You want to carry forward capital losses to offset future gains

- You have other Indian income beyond stock gains — rent, interest, dividends

Filing in India also creates a clean paper trail that strengthens your DTAA credit claim in your country of residence. Most NRI tax CAs recommend filing ITR-2 annually regardless of refund eligibility — the administrative cost is low and the compliance benefit is high.

For a full walkthrough of ITR filing as an NRI, read our guide on how NRIs can file income tax in India. For repatriation of your post-tax proceeds, read our guide on NRI repatriation of investment returns.

Repatriating Your Stock Market Profits — What You Need to Know

Earning returns in India is only half the equation. For most NRIs, the goal is to bring those profits home — and the rules governing this are clear, provided you have set up the right account structure from the start.

Repatriation From Your NRE-PIS Account

When you sell shares held through an NRE PIS account, the proceeds flow back directly into your NRE account and can be freely repatriated — both your original capital and your profits. Tata AIA There is no annual cap, no RBI approval required, and no additional documentation beyond what your bank already holds. This is the single biggest advantage of the NRE-PIS structure and the primary reason most long-term NRI investors choose it.

The only condition: the funds must be repatriated to your own overseas bank account. You cannot repatriate directly from your NRE account to a family member’s foreign account — transfer to your own linked overseas account first, then make any onward transfers from there. Khaleej Times

Repatriation From Your NRO Account

NRIs can repatriate up to USD 1 million per financial year from their NRO account, covering all sources of Indian income including stock sale proceeds, rental income, dividends, and pensions combined. Mintbyte This is not a per-category limit — it is an aggregate annual ceiling across everything flowing out of your NRO account.

The USD 1 million limit resets on April 1 every financial year. If you need to repatriate more than this amount, you must apply to the RBI through your authorised dealer bank — approval is granted case by case, typically for specific reasons such as medical emergencies or education expenses.

Documents Your Bank Will Require

The documentation differs depending on your account type:

For NRE account repatriation:

- Passport copy

- NRE account statement

- Form A2 — a FEMA declaration confirming the repatriation is in compliance with RBI guidelines

For NRO account repatriation:

- Form 15CA — a self-declaration filed on the Income Tax India portal confirming that applicable taxes have been paid Axis Max Life Insurance

- Form 15CB — a certificate from a Chartered Accountant verifying tax compliance before the transfer is processed

- Form A2 — FEMA declaration

- Bank request form with source of funds details

⚠️ The most common reason banks reject NRO repatriation requests is missing or incorrectly filed Form 15CA/15CB. Have your CA prepare these before initiating the transfer — not after.

A Note on Planning Large Repatriations

If your annual stock gains from an NRO account are likely to exceed USD 1 million, plan your repatriation across two financial years. The reset date of April 1 means a transfer in March and a follow-up transfer in April effectively doubles your available limit across two financial years without requiring any special RBI approval. Khaleej Times This is a straightforward and entirely compliant strategy that experienced NRI investors use regularly.

For a full walkthrough of the repatriation process including property and fixed deposit proceeds, read our detailed guide on NRI repatriation of investment returns from India.

5 Common Mistakes NRIs Make When Investing in Indian Stocks

The setup process is straightforward when done correctly. The problems arise when NRIs either rush through it or rely on outdated information. These are the five mistakes that cause the most compliance headaches — and the most avoidable financial loss.

Mistake 1: Continuing to Use a Resident Savings Account After Becoming an NRI

This is by far the most widespread FEMA violation among new NRIs. RBI regulations mandate that once you qualify as an NRI, you must convert your resident savings account to NRE or NRO within 30 days. Continuing to use a resident account makes all transactions illegal and can attract penalties up to ₹2 lakh — and banks are required to report non-compliance to authorities. Tata AIA

The dangerous part is that many NRIs operate this way for months or even years without receiving any notice — until they try to repatriate funds, sell a property, or face a tax audit. By then, the cumulative liability can be significant.

Fix it: Notify your bank the moment your residential status changes. Most major banks — HDFC, ICICI, SBI, Kotak — allow online conversion without visiting a branch in India.

Mistake 2: Investing in Stocks Without PIS in Place

Some NRIs attempt to buy listed Indian stocks directly through their NRO account without PIS permission, assuming it is a minor procedural step they can sort out later. It is not. Trading in Indian equities without PIS in place is a direct FEMA violation — penalties can reach three times the contravention amount or ₹2 lakh, whichever is higher, plus ₹5,000 per day for every day the violation continues. IndiaStat

Fix it: Never place a single stock trade until your PIS permission letter is in hand and your four-account linkage is confirmed in writing by your broker.

Mistake 3: Attempting Intraday or Short-Sell Trades

NRI trading accounts look identical to resident trading platforms. The buy and sell buttons are in the same place. This leads some NRIs to assume they can trade intraday — buying and selling the same stock within the same session. They cannot. Intraday trading and short selling are strictly prohibited for NRIs under SEBI and RBI regulations. Only delivery-based trades are permitted. Mintbyte

Most NRI-enabled brokers have platform-level blocks in place — but not all do. If your broker does not have this safeguard and you accidentally execute an intraday trade, report it to your broker immediately. Voluntary disclosure is treated significantly more favourably than a regulatory flag.

Fix it: Confirm with your broker in writing that your account is configured to allow delivery-based trades only.

Mistake 4: Missing FATCA/CRS Declarations — Especially for US and Canada NRIs

NRIs based in the United States, Canada, the United Kingdom, Australia, and approximately 100 other countries are subject to automatic financial information exchange between India and their country of residence. FATCA and CRS declarations are mandatory for NRIs in these jurisdictions — without them, your bank and broker cannot open or maintain your investment accounts. IBEF

For US-based NRIs in particular, non-declaration creates serious exposure — the IRS receives information on Indian account balances directly from Indian financial institutions. Gaps in reporting trigger international tax scrutiny, not just Indian compliance issues.

Fix it: Submit your FATCA/CRS declaration at the time of account opening. Update it every time your tax residency status, address, or Tax Identification Number (TIN) changes.

Mistake 5: Not Tracking the 10% Individual Investment Cap

With Budget 2026 doubling the individual NRI cap from 5% to 10%, many NRIs are now able to build much larger positions in individual Indian companies. However, the cap still exists — and breaching it is a FEMA violation regardless of intent.

Most NRIs investing in large-cap stocks will never come close to the 10% ceiling. But for NRIs building concentrated positions in mid-cap or small-cap companies — where the paid-up capital base is smaller — this ceiling can be reached faster than expected. Your broker’s platform should flag when you approach the limit, but do not rely solely on automated alerts.

Fix it: If you are building a significant position in any single listed company, periodically check the company’s shareholding pattern on BSE or NSE to monitor aggregate NRI holdings. If the aggregate is approaching 24%, purchases by all NRIs will be suspended automatically by the exchange — you will not be able to add to your position until it drops below the threshold.

For a comprehensive look at the full Indian investment landscape as an NRI, read our guide on how to invest in India as an NRI and understanding the Indian stock market for beginners.

Frequently Asked Questions — NRI Investment in Indian Stock Market

Q: Can NRIs invest in the Indian stock market? A: Yes. NRIs, OCI cardholders, and PIOs can legally invest in Indian listed equities through the RBI’s Portfolio Investment Scheme (PIS) or the Non-PIS route. You need an NRE or NRO bank account, PIS permission from a designated bank, and a linked demat and trading account with a SEBI-registered broker. Intraday trading and short selling are not permitted.

Q: What is the Portfolio Investment Scheme (PIS) for NRIs? A: PIS is an RBI-regulated framework that allows NRIs and OCI cardholders to buy and sell shares and convertible debentures of listed Indian companies on recognised stock exchanges. All transactions flow through a single designated NRE or NRO bank account, with TDS automatically deducted at source on any gains. Every transaction is reported to the RBI by your bank.

Q: Do NRIs need a special bank account to invest in Indian stocks? A: Yes. You need either an NRE (Non-Resident External) or NRO (Non-Resident Ordinary) account with a bank designated by RBI to offer PIS services. Your regular resident savings account cannot be used once you become an NRI — using it is a FEMA violation. Major PIS-designated banks include HDFC, ICICI, Kotak, Axis, SBI, and IndusInd.

Q: What is the difference between NRE and NRO accounts for stock trading? A: An NRE account holds foreign-earned income converted to rupees and offers full repatriation of both capital and profits with no annual cap. An NRO account holds income earned within India and allows repatriation of up to USD 1 million per financial year. For long-term NRI equity investing with the intent to bring profits home, the NRE-PIS route is generally more suitable.

Q: Can OCI cardholders invest in Indian stock markets? A: Yes. OCI cardholders are treated largely on par with NRIs for equity investment purposes and can participate in PIS under the same individual and aggregate investment caps. However, like NRIs, OCI cardholders cannot invest in agricultural land, plantation property, or prohibited sectors under FEMA. PIOs without OCI status may face additional documentation requirements.

Q: How much can an NRI invest in a single Indian company? A: Following Budget 2026 reforms, an individual NRI or OCI can hold up to 10% of the paid-up capital of any single listed Indian company — doubled from the earlier 5% limit. The aggregate cap for all NRIs and OCIs combined in a single company is 24% of paid-up capital. Breaching these limits is a FEMA violation regardless of intent.

Q: Can NRIs do intraday trading in Indian stock markets? A: No. Intraday trading is strictly prohibited for NRIs under SEBI and RBI regulations. NRIs can only trade on a delivery basis — meaning you must take ownership of shares you buy and hold them for at least one trading day before selling. Attempting intraday trades can result in the transaction being reversed and your account flagged for FEMA non-compliance.

Q: Can NRIs trade Futures and Options (F&O) in India? A: Effectively no through the standard PIS route. NRIs may participate in derivatives only under very strict conditions — margins must be brought from abroad, positions must be closed before expiry, and individual broker and exchange approval is required. Most NRI broker platforms do not offer F&O access. Currency derivatives and commodity trading are also restricted for NRIs.

Q: What documents does an NRI need to open a demat and trading account in India? A: You will need a valid passport with visa page, PAN card, overseas address proof (driver’s licence, utility bill, or bank statement not older than 3 months), Indian address proof, cancelled cheque or bank statement from your NRE/NRO account, PIS permission letter, passport-sized photograph signed across the face, and a FATCA/CRS declaration if you reside in the USA, UK, Canada, Australia, or other CRS-member countries. All documents must be attested by an Indian Embassy, notary, or overseas branch of an Indian bank.

Q: How is tax calculated on NRI stock market gains in India? A: Short-term capital gains (shares held under 12 months) are taxed at 20%. Long-term capital gains (shares held over 12 months) are taxed at 12.5% on gains exceeding ₹1.25 lakh per financial year. TDS is automatically deducted by your PIS bank at the point of sale. NRIs do not receive the basic exemption limit of ₹2.5 lakh that resident Indians get on capital gains.

Q: How do NRIs avoid double taxation on Indian stock market gains? A: India has DTAA agreements with over 90 countries including the USA, UK, UAE, and Canada. Under DTAA, you can claim a credit in your country of residence for taxes already paid in India — or pay tax only in India if your country of residence has no capital gains tax, such as the UAE. To claim DTAA benefits, you must submit a Tax Residency Certificate (TRC) from your country’s tax authority and file Form 10F on the Indian Income Tax portal.

Q: Do NRIs need to file an income tax return in India for stock market gains? A: Not always — if correct TDS has been deducted, filing is not mandatory. However, filing an ITR is strongly recommended if your TDS deducted is higher than your actual tax liability (to claim a refund), if you want to carry forward capital losses to offset future gains, or if you have other Indian income beyond stock gains. Filing ITR-2 annually also creates a clean compliance record and supports your DTAA credit claim abroad.

Q: Can NRIs repatriate stock market profits out of India? A: Yes, subject to which account the proceeds flow into. Proceeds from an NRE-PIS account are fully and freely repatriable with no annual cap. Proceeds from an NRO account can be repatriated up to USD 1 million per financial year across all Indian income sources combined. NRO repatriation requires Form 15CA and Form 15CB prepared by a Chartered Accountant before the bank processes the transfer.

Q: Can I invest in Indian stocks as an NRI without visiting India? A: Yes. Most major banks and SEBI-registered brokers now offer fully online NRI account opening with Video In-Person Verification (V-CIP), eliminating the need to visit India. Document attestation can be done at your nearest Indian Embassy or Consulate, or by a notary abroad. Once accounts are set up, all trading, fund transfers, and monitoring can be done remotely from anywhere in the world.

Q: What happens to my existing resident demat account when I become an NRI? A: Your existing resident demat account must be converted to an NRI demat account — either repatriable (linked to NRE) or non-repatriable (linked to NRO). You cannot continue operating a resident demat account after your status changes to NRI. Shares held in your resident account are transferred to your new NRI demat account. Similarly, your resident savings account must be converted to NRO or closed — it cannot be converted directly to NRE.

Q: Can NRIs invest in IPOs in India? A: Yes. NRIs can apply for IPOs in India using their NRE or NRO bank account without needing PIS permission specifically for the IPO application. IPO allotments are credited to your NRI demat account. Refunds for unsuccessful applications are credited back to the same NRE or NRO account. Note that some IPOs may restrict NRI participation — always check the offer document before applying.

Q: How many PIS accounts can an NRI have? A: Only one. RBI regulations allow an NRI to hold PIS permission with only one designated bank at a time — either an NRE-PIS or NRO-PIS account. If you wish to switch your PIS to another bank, you must first surrender the existing PIS permission before the new bank can apply for a fresh one on your behalf. Having PIS with more than one bank simultaneously is a compliance violation.

Q: Are NRI stock market investments in India safe from a legal standpoint? A: Yes, provided you follow the correct setup — PIS permission, designated NRE/NRO account, SEBI-registered broker, and valid KYC. The framework is well-established under FEMA 1999 and backed by RBI and SEBI oversight. The risks are market risk (stock price fluctuations) and currency risk (INR/foreign currency movement) — not legal risk, as long as you stay compliant. Always use a SEBI-registered broker and avoid prohibited sectors.

Q: What is the difference between a repatriable and non-repatriable NRI demat account? A: A repatriable NRI demat account is linked to your NRE bank account, and the proceeds from selling shares can be freely sent back to your overseas account with no annual cap. A non-repatriable NRI demat account is linked to your NRO bank account, and repatriation is capped at USD 1 million per financial year across all Indian income. Most NRIs who invest with foreign earnings prefer the repatriable structure for maximum flexibility.

Q: Can NRIs invest in Indian ETFs and index funds? A: Yes. NRIs can invest in equity ETFs and index ETFs listed on BSE or NSE through the PIS route on a delivery basis. Commodity ETFs and currency ETFs are not permitted. For index exposure without stock-picking, equity ETFs tracking indices like Nifty 50 or Sensex are a straightforward option. Alternatively, NRIs can invest in index mutual funds through the Non-PIS route — no PIS permission is needed for mutual fund investments.

Ready to Start? Your Next Steps

Investing in Indian stock markets as an NRI is entirely achievable — the framework is well-established, the process is online-friendly, and the opportunity in 2026 is backed by genuine regulatory momentum. The key is setting up the right structure from the beginning rather than patching it together later.

Here is what to do next, in order:

- Get your PAN card if you do not already have one — it is mandatory for every step that follows. Read our guide on how to apply for a PAN card as an NRI.

- Open your NRE account with a PIS-designated bank — HDFC, ICICI, Kotak, Axis, or SBI are all reliable starting points. Read our NRI bank account guide if you need help choosing.

- Apply for PIS permission through your bank — this is a 2 to 5 day process once your NRE account is active.

- Choose a SEBI-registered broker that explicitly supports NRI accounts and open your demat and trading account.

- Consult a SEBI-registered investment advisor or NRI-specialist CA before placing your first trade — especially if you are based in the USA or Canada where FATCA reporting adds a layer of complexity.

If you are new to the Indian market altogether, start here: understanding the Indian stock market for beginners. And if you want a lower-maintenance alternative to direct stock picking, explore NRI mutual fund investments in India — the compliance setup is simpler and the diversification is built in.

Last updated: March 2026. Regulations may change — always verify with a qualified NRI financial advisor or CA.